Arm’s AI data center business is strong, with performance guidance slightly above expectations.

On May 6, after the U.S. stock market closed, Arm announced its Q4 fiscal year 2026 earnings, reporting a 20.2% year-over-year revenue increase to $1.49 billion, with adjusted earnings per share of $0.60, both exceeding analyst expectations.

Arm expects Q1 revenue to be approximately $1.29 billion, with adjusted earnings per share between $0.36 and $0.44, all higher than previous analyst forecasts.

Arm expects Q1 revenue to be approximately $1.29 billion, with adjusted earnings per share between $0.36 and $0.44, all higher than previous analyst forecasts.

Management noted that the demand for high-efficiency CPU designs in AI data centers continues to rise, effectively offsetting short-term pressures in the smartphone market. The company also revealed that demand for its AGI CPU products has exceeded $2 billion for the fiscal years 2027 to 2028.

However, the company did not raise its revenue expectations, citing uncertainties about whether the supply chain can meet demand. After hours, Arm’s stock initially surged by 10% before quickly dropping, closing down about 6% as of 7 PM New York time.

Revenue and Profit Exceed Expectations, Setting Annual Records

Arm’s Q4 revenue of $1.49 billion, a 20% year-over-year increase, not only surpassed market consensus but also performed stronger than the company’s previous high guidance.

CFO Jason Child stated that this quarter’s revenue was nearly $250 million higher than the previous record, indicating that Arm is accelerating its benefits from the AI and high-performance computing cycle.

Profitability also showed strong performance:

- Q4 adjusted earnings per share were $0.60, higher than the market expectation of $0.58.

- Annual adjusted earnings per share were $1.77.

- The adjusted operating profit for Q4 was $731 million, with an adjusted operating margin of about 49%.

However, profit margins have come under some pressure. Last year, Arm’s adjusted operating margin was about 53%, which has decreased to approximately 49% this fiscal year.

This primarily reflects the company’s increased investment in research and self-developed chips, with adjusted operating expenses for Q4 reaching $734 million, a 30% year-over-year increase.

In other words, Arm is transitioning from a light-asset IP licensing company to a model that integrates “IP + self-developed chips,” which brings greater market space but also higher costs.

Licensing Revenue Shines, Clients Bet on Next-Generation Architecture

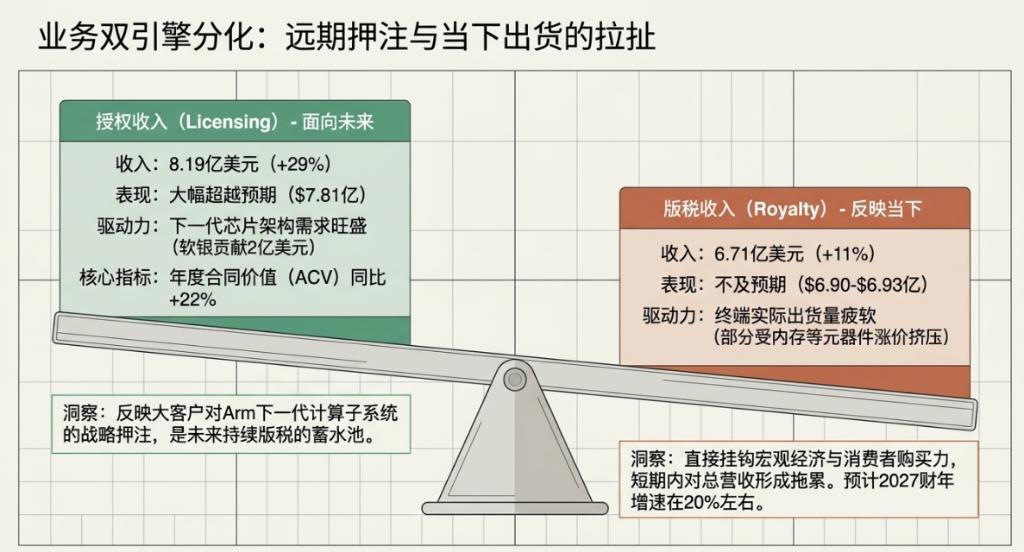

This quarter, licensing revenue was particularly outstanding. Q4 licensing revenue reached $819 million, a 29% year-over-year increase, significantly exceeding analyst expectations of $781 million.

CFO Jason Child attributed this to strong demand for next-generation chip architectures and deep strategic collaborations with clients, including a long-term strategic cooperation agreement with the Indonesian government and two new generation computing subsystem (CSS) licensing agreements.

Notably, SoftBank’s technology licensing and design service agreements contributed $200 million in licensing revenue this quarter.

Licensing revenue is one of the best indicators of “future demand” in Arm’s business model. Clients purchasing Arm architectures and IP licenses often indicate that they will launch chip products based on Arm technology in the coming years, leading to ongoing royalty income for Arm.

Licensing revenue is one of the best indicators of “future demand” in Arm’s business model. Clients purchasing Arm architectures and IP licenses often indicate that they will launch chip products based on Arm technology in the coming years, leading to ongoing royalty income for Arm.

Thus, the significant growth in licensing business indicates that major clients are still expanding their investments in the Arm ecosystem.

Arm also cautioned that licensing revenue itself can exhibit quarterly fluctuations, depending on the timing of large transactions, so the company places greater emphasis on annual contract value. In Q4, Arm’s annual contract value increased by 22% year-over-year, still above the company’s long-term growth expectations.

Royalty Business Below Expectations, Smartphone Market Weakness a Short-Term Drag

In contrast to the licensing business, royalty revenue showed some weakness.

Q4 royalty revenue was $671 million, an 11% year-over-year increase, but below market expectations of approximately $690 million to $693 million.

Royalty revenue is more directly related to actual shipment volumes. After Arm clients ship chips using its architecture or IP, Arm receives royalties based on shipment volumes. Therefore, lower-than-expected royalties typically indicate that some end-market shipments are not strong enough.

The primary drag came from smartphones. Haas noted that smartphone unit growth “turned negative” last quarter, with weakness concentrated in the low-end market. As Arm has long been deeply tied to the smartphone ecosystem, cyclical fluctuations in the smartphone market will still impact the company’s short-term revenue.

Recent tight supply of memory components may drive up end-device prices, further affecting smartphone shipment volumes and royalty revenues tied to those volumes. Mobile chip supplier Qualcomm also conveyed a similar signal in its earnings outlook.

However, management emphasized that high-end smartphones and AI data centers are offsetting the weakness in low-end smartphones. Notably, royalty revenue from data centers more than doubled year-over-year, becoming the fastest-growing part of the royalty business.

The company expects royalty revenue growth for the full fiscal year 2027 to be around 20%.

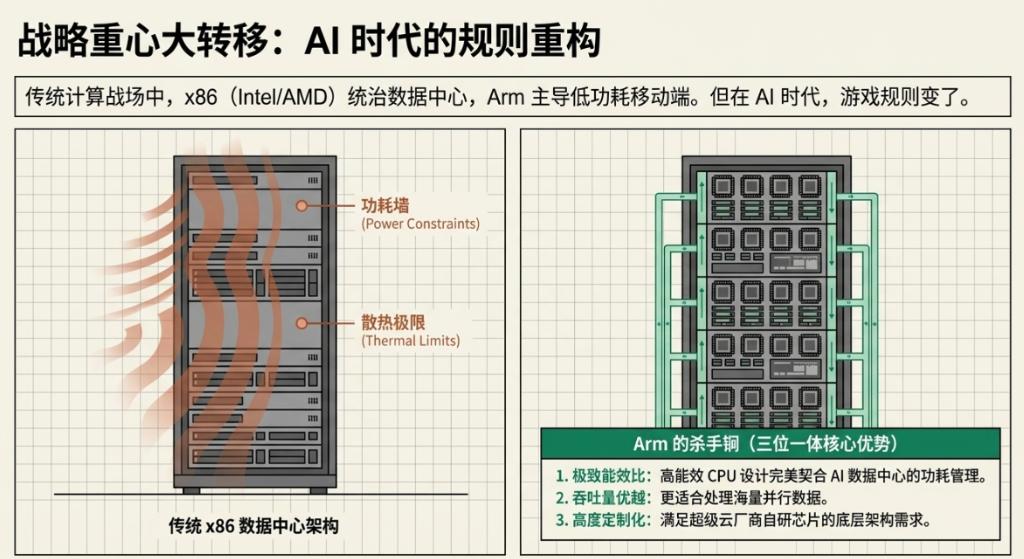

AI Data Centers as a New Growth Engine, Arm Challenges x86’s Traditional Advantages

Arm’s long-term narrative is shifting from smartphones to data centers.

Management stated that an increasing number of designs based on Arm architecture are entering AI data center deployments, where power control and thermal management have become increasingly prominent constraints, highlighting the competitive advantages of Arm’s high-efficiency CPU designs.

Historically, Arm architecture has been known for low power consumption, dominating mobile devices like smartphones and tablets. In the server and PC markets, the x86 architecture used by Intel and AMD has long held dominance.

Historically, Arm architecture has been known for low power consumption, dominating mobile devices like smartphones and tablets. In the server and PC markets, the x86 architecture used by Intel and AMD has long held dominance.

However, in the AI era, the importance of energy efficiency, core count, throughput, and customization is rapidly increasing, and Arm’s penetration in data centers is accelerating.

The Arm AGI CPU released in March this year has garnered significant attention from clients. Currently, all three major cloud providers have launched or adopted Arm architecture CPUs:

- Amazon AWS continues to expand Graviton, integrating it with infrastructure like Trainium and Nitro;

- Google has launched the Axion CPU, pairing it with TPU training and inference chips;

- Microsoft Azure is advancing its self-developed Arm CPU, Cobalt;

- NVIDIA’s AI server systems also extensively use Arm architecture CPUs, such as Grace/Vera-related products.

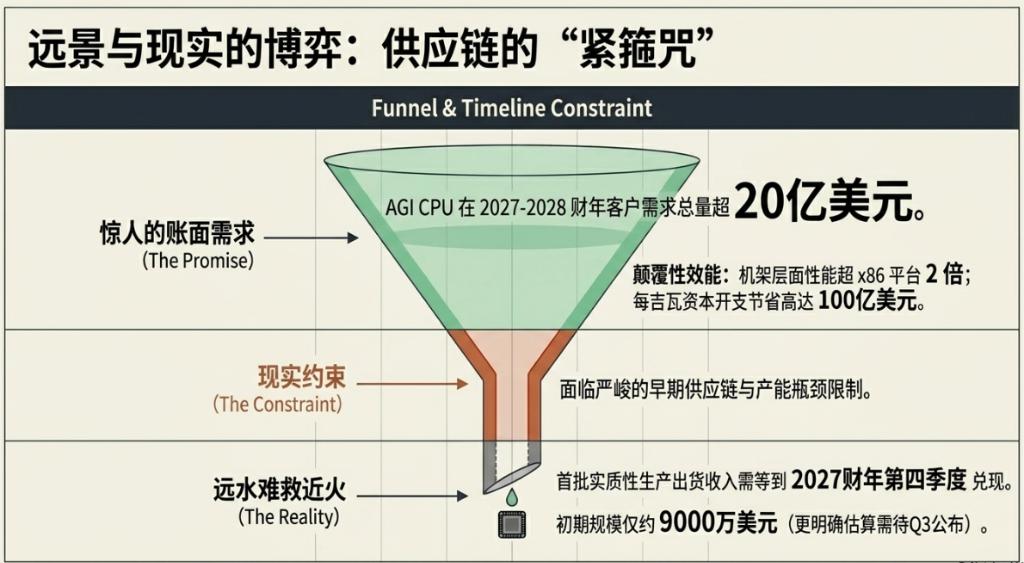

The company disclosed that demand for AGI CPU products has exceeded $2 billion for the fiscal years 2027 to 2028. Arm also stated that its AGI CPU is expected to achieve more than double the performance compared to x86 platforms at the rack level and help AI data centers reduce capital expenditures by up to $10 billion per gigawatt.

However, Arm also cautioned that the AGI CPU currently faces supply constraints, which somewhat limits the actual shipment scale in the short term.

Initial production shipment revenue is expected to appear in Q4 of fiscal year 2027, with a scale of approximately $90 million, and the company anticipates providing a clearer estimate in Q3.

Initial production shipment revenue is expected to appear in Q4 of fiscal year 2027, with a scale of approximately $90 million, and the company anticipates providing a clearer estimate in Q3.

Guidance Slightly Above Expectations, But Not Enough to Support Stronger Valuations

Arm’s guidance for the current quarter is slightly above market expectations.

- The company expects a midpoint revenue of $1.26 billion for Q1, higher than analyst expectations of $1.25 billion;

- The midpoint adjusted earnings per share is expected to be $0.40, also above market expectations of $0.36 to $0.37.

Management expects Q1 royalty and licensing revenue growth rates to both be around 20% year-over-year.

For the full year, licensing revenue is expected to be more skewed towards the second half, with about 60% occurring in the second half and 40% in the first half. Operating expenses are expected to grow a few percentage points quarter-over-quarter, reflecting that Arm is still in the phase of increasing research and chip investments.

Analysts believe that in the context of high valuations, “slightly exceeding expectations” is clearly not enough. Arm’s stock price has surged over 100% this year, and the day before the earnings report, it rose 13.6% due to AMD’s upward revision of the server CPU market outlook.

Currently, Arm’s forward P/E ratio is about 95 times, far exceeding the S&P 500’s level of about 21 times.

Comments

Discussion is powered by Giscus (GitHub Discussions). Add

repo,repoID,category, andcategoryIDunder[params.comments.giscus]inhugo.tomlusing the values from the Giscus setup tool.